Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

I didn’t actually see much Web-TV as I had expected to (see previous blog), but several IBC 2012 write-ups I have read so far, including those from people I respect like Giles Cottle or John Moulding have said say that there was no new “big thing” this year. I disagree or otherwise, there never is anything radically new – it depends on your point of view. Below is what I picked up as genuine game changers:

The Telia Soneria STB shrunk into a Samsung TV app is a true paradigm shifter.

VO’s second screen “Deep” app is also a breakthrough innovation; with the “doh-why-didn’t-I-think-of-that” magazine approach to content browsing.

Sony's 4K consumer TV hit me in the stomach just as hard as when I first saw an HD display about ten years ago.

Huge progress in the way data can be extracted from devices with extensions to the TR-069 protocol shown at the ADB, the SoftAtHome or the Mariner Partner’s stands to name just a few (bit expect more detailed reports after BBWF next month).

All this data will need to be crunched, paving the way to a major 2013 theme, which will be Big Data.

NDS showed their Solar project that is all about bringing this Big Data approach to TV. Project Fresco (ex project Surfaces) was also being demoed behind closed doors, and even if it's hard to see this impacting the market for many years, it is a mind blowing demo using a massive 6k display.

In my forthcoming write-up also expect an update on Verimatrix’ never ending successes, a sexy start-up called Klia with a CRM product delivering part of the Big Data promise before anyone else, HEVC news or lack thereof, Kit digitals strong attempt to reassure and updates on Zappware, Harmonic, Capablue, Visual Unity, Broadpeak, never.no, Corpus Media labs.

If one of these subjects is of more relevance to you than others, let me know, I’ll be sure to cover it more thoroughly … detailed write-up coming soon.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

This is the final-preparations-for-IBC time of year. So In speaking with friends and colleagues, David Gillies, who runs isis digital, told me about some of the streaming companies he was planning to see. David feels there is some matchmaking to do between them and the T2 and T3 operators. Only the big T1s can put together OTT strategies by calling all the shots. He’s right of course and that’s one area where independent consultants like us can bring value. But his plans for IBC 2012 sparked a moment of realisation in my mind that we were talking about something very familiar. Oh yes, wasn’t this kind of streaming supposed to happen like 15 years ago? Web TV was one of the drivers of the Internet bubble.

After NAB 2001, the next tradeshow I went to when I was still getting to grips with digital TV and what was becoming IPTV was « Narrowcast 2002 ». The Internet bubble had just finished bursting and the telecoms one was still exploding. Some of the first generation Web-TVs were still alive, although not really kicking anymore.

A bright young employee from TF1 that I spoke to on the show floor confidently predicted that this Internet nonsense would never take over TV - TV would take over the Web. His proof was that one of France’s highest traffic websites was his own one from TF1, France’s number one TV station (the conference was in Paris).

Since then all the Web TVs have died and faded into distant memory, but it doesn’t look like TF1 benefited much. In fact TF1’s TV market share has lost about 50% in the last 10 years and despite remaining an attractive Web property, they haven’t compensated the broadcast losses with Web traffic however which way you measure it.

First generation Web TV had two flaws in their business plans, either of which could sink any initiative, however much money they raised and raised again. Firstly of course, the network just wasn’t ready during the Internet & Telecoms bubbles at the end of the last century. Not only do you need broadband, but you need it in multiple megabits per second not in the hundreds of kilobits per second of early broadband.

But more importantly, the overriding concept « Content is King » still wasn’t really understood throughout the telecoms industry or with many start-ups. Traditional players like my friend at TF1 had a stranglehold on any content that might draw a big and regular audience. Ten years on, User Generated Content or UGC, one of the early Web TV’s promises to replace prime time content, is still only just taking a sliver out of the hours-consumed-per-day pie charts.

In 2012, the next big thing is called the cloud. For anyone remembering Larry Ellison’s vision of a Net computer dating even further back than my Narrowcast conference, this should start sounding a bit déjà vu, non?

A powerful, fast, responsive and service enabled network with simple devices to consume directly from it. Hey, not only is that going back to the mainframe computing model, but it’s also mimicking the broadcast paradigm to a certain extent, just without the broadcast technology. In his 2009 book called The Big Switch (Rewiring the world, from Edison to Google) Nicolas Carr used the commoditization of electricity a century ago as a parallel to what IT infrastructure is currently transforming into with Cloud computing. In the heyday of the Industrial revolution, any industrial project had an electricity generating part to it. It would have been unthinkable otherwise. In the same way broadcasters have today installed a huge amount of kit in peoples homes and find it often unthinkable to do otherwise. But if that kit, otherwise know as Customer Premise Equipment or CPE, were to be commoditized into the Cloud so any humble device could receive the service, wouldn’t that be just what Web TV was all about?

The two Web TV killers of ten years ago are gone: sufficient broadband penetration will now support a monetized business as any Netflix subscriber user can show. Content owners saw what happened to a music industry that tried to ignore then resist the Web and are now more responsive. They will actually talk to network operators, and even the Hollywood majors will experiment new things (OK only small, low-risk things but it’s a marked improvement on their head-in-the-sand policy of 10 years ago).

So now is the time for Web TV to rise from the ashes like a Phoenix. But rather than a mythical return, my friend David Gillies & I are convinced this time it will turn into a real and sustainable challenge to the existing broadcast TV market. The market moves so much faster than it used to and I’m sure we’ll know if we’re right by the time we prepare for IBC2013. But ponder on your way to IBC this year if you have figured out how to use the Web TV 2.0 to your advantage.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

Nice infographic from ONLINECOLLEGES.COM

It's a bit US-centric, but then so is the whole chord-cutting debate. Good food for thought in any case.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l’utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

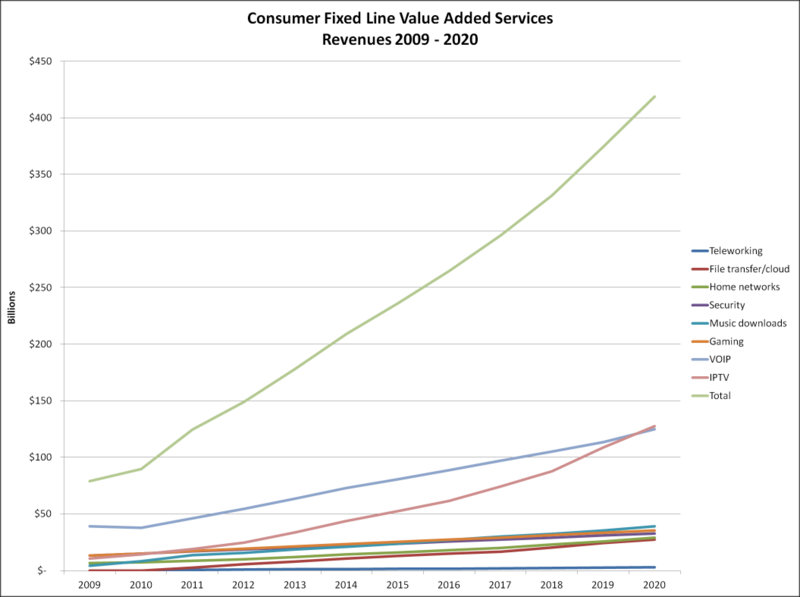

According to Oliver Johnson, CEO of Point Topic, Consumer Value Added Services (VAS) Revenues are to Triple to $420 Billion in 2020. Wow! Tripling in 10 years is a compound annual growth rate of about 14%.

Johnson used the following graphic during a presentation at CommunicAsia 2012 earlier this week:

Point Topc's take on 2020 VAS revenues

Source Point Topic (CommunicAsia 2012)

Who wouldn’t want to operate within such an industry?

That got me thinking, who indeed?

Much of what makes up these VAS aren’t yet in the scope of global juggernauts Apple & Google. On the contrary, all seem to be very Network operator centric.

So why then are my friends at major European Telcos so gloomy?

Point Topic have looked at current VAS and projected them to 2020. That’s a good approach to get an idea of market size, but doesn’t show who’ll be selling the services by 2020 i.e. in an IP lifetime.

Let’s run through Point Topic’s 8 VAS:

1. IPTV – this may still be Telco’s exclusive hunting ground but as I just wrote in a white paper, IPTV is being complemented with OTT. By 2020 there will be no distinction between IPT & OTT. If Google and Apple take too long to get their TV acts together the Netflix’ of the world will have carved out a big piece of this pie for themselves. Otherwise for Telcos to stand a chance of staying on top of this market, they’ll need the support of regulators and crazy laws like ACTA to exterminate what’s left of Net Neutrality.

2. VoIP – again what could be construed as Telco hunting ground, is already dominated globally by the likes of Skype so isn’t voice is destined to become free? I asked Point Topic to explain why they see so much VoIP revenue in 2020. Oliver told me “VoIP currently has the largest share of fixed line consumer VAS & will still grow slowly (see chart).” So what about free VoIP? “While operators are offering free VoIP, it’s often only free to other VoIP connections and sometimes only to users on the same ISP. There are still going to be plenty of calls to mobile and standard fixed phones and along with those ISPs that do charge for VoIP as part of a bundle this still adds up to a pretty good revenue stream”.

3. Gaming – Gaming is classified as just another VAS, but this industry obeys its own complex rules. Most gaming industry pundits believe that the big editors like EA or Valve will lose out to more innovative smaller outfits. Operators have been trying to capture some of the value here for over a decade. I don’t see why they should be any more successful in the future than in the past.

4. Music downloads – I’m surprised that this market is still seen as existing by Point Topic. At the last party with dancing, that I went to, people asked for a Deezer connection to play their songs, rather than hooking up their iPhone. To justify downloading, the size of files must be large relative to available bandwidth. If there are say, stereoscopic 4k videos in 2020, then maybe video downloading will still exist, but I don’t see how downloading will remain relevant for sound files in 2020. So if this revenue is generated from streaming, then network operators might just scrounge the scraps, with the lion’s share of this market remaining with service providers like iTunes or Spotify.

So I asked Point Topic why they kept this segment until 2020. Oliver answered: “streaming will become more popular, but it can still be patchy. Unless you want to use your mobile bandwidth while out of reach of free WI-FI, or eat your much larger fixed allowance then just for efficiency’s sake, users will want to download once and share that file amongst their devices. Memory/disk space if just cheaper and more reliable than having to be in the cloud the whole time. In addition we still retain the desire to 'own' something, even if it's bits on your disk drive, having something to hand is more convenient and more desirable. Just look at the Megaupload case to see what can happen to your data if you trust it to someone else.”

That’s where I beg to differ, because I think connectivity will be so much better and even more ubiquitous in 2020.

5. Security – I have no doubt that there will be a gold rush on this market. Of course anyone selling spades will make a fortune, but beyond the obvious B2B market, the jury is still out as to whether the public at large will spend significant budget on remote sensors, cameras, and the like. If the segment were to include home automation, it might stand a better chance. But it’s still a level playing field so anyone could come out on top.

6. Home networks – this is a new frontier, which I’m excited about. People are in pain and we don’t even know how to start fixing their problems. Part of the solution will include more robust and simple networking technologies, some monitoring and helpdesk services, content discovery and DLNA approaches to in-house content sharing. But if home networking can’t be made easy very soon, it may never make it as a mass market, because the Cloud is already here...

7. File transfer / cloud – I would have guessed this would be the big one in a 2020 market. Watching Dropbox make an impact in both business and consumer segments in parallel shows that there is a clear demand here. In an 8-year window I could easily imagine the descendants of Dropbox taking a slice out of whatever I’m willing to pay for access to content. Amazon seams to believe in the link between hosting services and the content therein. The experts at Point Topic have plotted a line based on today’s typical file transfer service. Again I have no issue with the method to get to a market size, but this is an area where services in 8 years will be so very different, that it probably doesn’t mean much anymore.

8. Teleworking – Teleworking was always going to be so very important so very soon. The technology has actually been available for many years. The success or otherwise of teleworking will now be driven by what is socially and / or professionally acceptable in terms of behaviour and work ethics more than by any new service or technology. So I see no reason for the tiny size or the stakeholders of the Teleworking market to change over what is - for social change - a short period of time.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l'utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

Short version of the June 2012 Viaccess-Orca (now VO), Harmonic and Broadpeak White Paper on the technical challenges and business imperatives of OTT.

Désolé, cet article est seulement disponible en Anglais Américain. Pour le confort de l'utilisateur, le contenu est affiché ci-dessous dans une autre langue. Vous pouvez cliquer le lien pour changer de langue active.

Long version of the June 2012 Viaccess-Orca (now VO), Harmonic and Broadpeak White Paper on the technical challenges and business imperatives of OTT.